The airline industry is one part of the broader aviation industry. It includes businesses that offer air transportation services for both passengers and cargo. The US, India, China, and the European Union are some of the most important markets for air travel, with the US domestic market being the world’s largest air travel market. Delta Air Lines, American Airlines, Lufthansa, and United Airlines, are among the largest and most profitable airlines in the world.

Over the last couple of years, with the global economy becoming more and more connected, air travel has been one of the fastest-growing transportation sectors. However, the COVID-19 pandemic hit the airline industry hard, erasing almost two decades of growth. The market size shrunk to $359.3 billion in 2020 from $818.32 billion in 2019. This drop in value of about 56% paralysed airlines, and the sector is expected to have a slow recovery. Pre-pandemic traffic levels aren’t projected to return until 2024. Now, with the ongoing Russia-Ukraine war, the airline sector is facing its second major crisis in recent times. The S&P 500 Airlines Index lost over 15% right after the invasion. Since then, the record-high increase in oil prices has also been having a direct impact on airlines. The sector is vulnerable to the uncertainty and volatility triggered by the war. However, now with oil prices stabilising, expectations of mask restrictions to be lifted, and easier access to new booster shots, airlines and their stocks are expected to start recovering.

QUICK TAKEAWAYS

- The airline industry includes all airline businesses that provide passenger and cargo services.

- COVID-19 severely impacted airlines but the industry turned out to be more resilient than when faced with previous economic shocks.

- Pandemic restrictions led to a decrease of 65.9% in air traffic and passenger numbers reduced by 2.7 billion in 2020.

- The US has four carriers, American Airlines, Delta Air Lines, United Airlines, and Southwest Airlines, that control about 80% of the domestic market.

- Airlines are primarily impacted by global events, oil prices, economic cycles, and M&As.

- Moving forward, the industry will be adopting new-age technologies and re-thinking its business models.

STATS CORNER

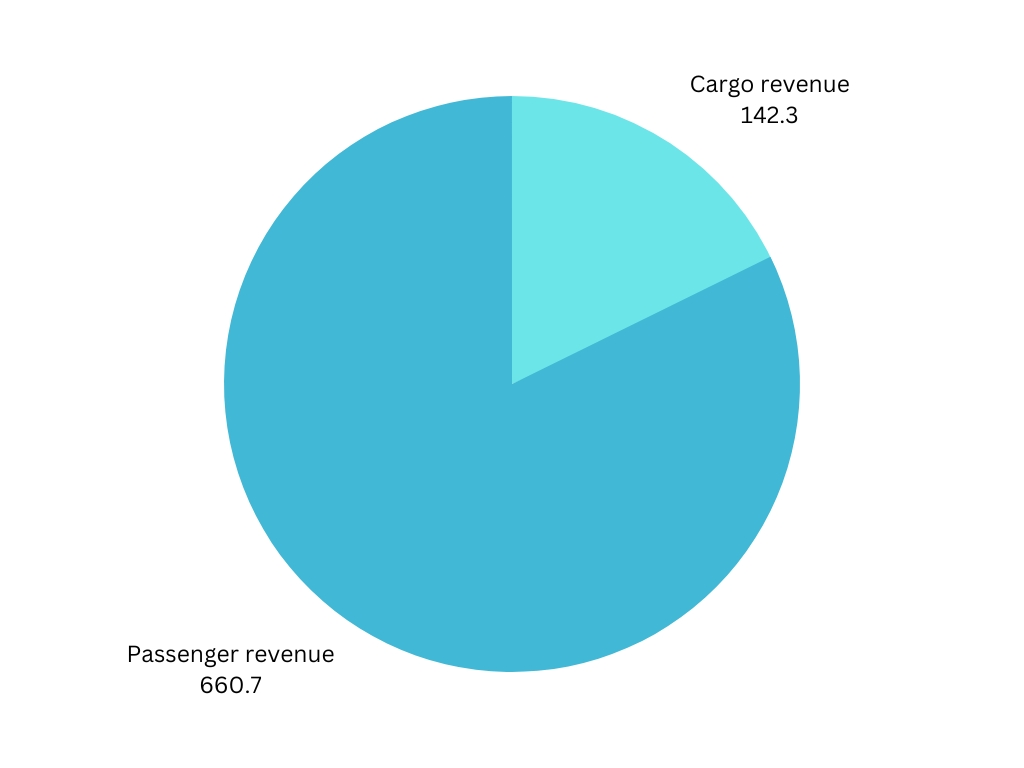

Estimated revenue for 2023 in billions of USD (Source)

GLOBAL AVIATION MARKET SIZE IN 2023

$333.96 billion

(Source)

PROJECTED GLOBAL AVIATION MARKET SIZE IN 2028

$386.21 billion

(Source)

KEY PLAYERS

[WORLDWIDE, BY MARKET CAP]

(Source | As of August 2023)

[THE UNITED STATES, BY REVENUE]

| Company Name | Revenue Generated | Revenue Generated | Revenue Generated | Revenue Generated | Revenue Generated |

| 2022 | 2021 | 2020 | 2019 | 2018 | |

| Delta Air Lines | $50.6B | $29.9B | $17.1B | $47.0B | $44.4B |

| American Airlines Group | $49.0B | $29.9B | $17.3B | $45.8B | $44.5B |

| United Airlines Holdings | $44.9B | $24.6B | $15.3B | $43.2B | $41.3B |

| Southwest Airlines | $23.8B | $15.8B | $9.0B | $22.4B | $22.0B |

| Alaska Air Group | $9.6B | $6.2B | $3.6B | $8.8B | $8.3B |

(Source: Macrotrends)

- Delta Air Lines (NYSE: DAL): One of the oldest legacy air carriers in the US, Delta Air Lines has 17.3% of the domestic market share in the US. Delta serves about 200 million customers every year, flying them across its global network of over 300 destinations across 50 countries.

- American Airlines Group (NASDAQ: AAL): American Airlines Group is the largest airline in the world based on fleet size and revenue passenger mile. It also has the biggest share in the domestic market in the US at 17.5% as of January 2023.

- United Airlines Holdings (NASDAQ: UAL): United Airlines Holding started as a mail service carrier airline in 1926 and, over the years, has grown to be one of the largest airlines in the US with a market share of about 15.6%.

- Southwest Airlines (NYSE: LUV): Southwest Airlines is one of the world’s leading low-cost carriers and has a market share of about 16.9% in the US. It offers its services at 121 airports across 11 countries.

- Alaska Air Group (NYSE: ALK): Alaska Air Group owns two airlines: Alaska Airlines, which is a mainline carrier, and Horizon Air, a regional carrier. Alaska Airlines holds about 6.2% of the US market share.

KEY DRIVERS

- Crude oil prices: The airline industry has a high reliance on crude oil, and hence, is highly sensitive to changes in crude oil prices. This is because fuel is one of the biggest expenses airlines have, and it makes up a significant portion of their gross costs. An increase in oil prices leads to an increase in the input costs, leading to a decrease in their profit margins and operational leverage. Usually, the stock prices of smaller airlines are more sensitive to oil price changes compared to legacy airlines. US airline stocks, though, are seen to be fairly resilient despite the oil price volatility, as observed during the Ukrainian crisis.

- Macroeconomic factors: Airline stocks tend to reflect the overall health of the economy. When the economy is slowing down, airlines generate lower revenues because the discretionary income falls, and consumers cut back on leisure air travel. Business air travel also reduces as companies look to cut costs. Conversely, when the economy is strong, discretionary incomes are higher, and the demand for air travel increases. This translates to higher revenues and stock prices for airlines. Foreign exchange rates also impact the profitability and stock values of companies in the sector. This is because the number of passengers changes with fluctuations in exchange rates. The demand for air travel goes down in a country with higher exchange rates because it gets more expensive for citizens of that country to afford air travel.

- Global events: The airline business is deeply interlinked with the global economy and hence global events, both positive and negative, have an almost immediate impact on the stock prices of airlines. For instance, terrorist attacks and wars make people cancel their travel plans due to safety concerns. This can have a short-term and a long-term impact on airlines. After the November 2015 Paris attacks, airline stocks saw a sharp decline in the short term but quickly reversed. However, post the 9/11 attacks in the US, airline stocks continued to drop over a longer period, and American Airlines dropped by over 90% over the year following the attacks.

- Mergers & Acquisitions: The business model of airlines makes it difficult for them to make money, and hence consolidation has been the key to saving the industry over the last few decades. Between 2001 and 2010, airlines in the US lost $55 billion and saw 20 airlines filing for bankruptcy protection. Amid such a crisis, consolidation helped the industry survive and recover. Today, four airlines control about 80% of the domestic market in the US. The European airline industry has also been considering consolidation since 2020. When there is a merger between two airlines, the stock prices of the companies merging see an increase in their stock price in the short term. In the long term, it’s been seen that mergers in the industry have a positive impact on the stock prices of other airlines in the industry as well because competition decreases.

WHAT DOES THE FUTURE HOLD?

Moving forward, airlines will be considering opportunities to boost their cargo services. Before the pandemic, several airlines had scaled down their dedicated cargo fleet because of low demand and unprofitability. However, cargo services ended up being the lifeline for many airlines during COVID-19. The cargo revenue went from 12% of the industry’s total revenue to 30% in 2020. This was primarily due to a surge in e-commerce, and this trend will continue. Airlines need to look at being agile and flexible and consider freighter conversions.

The industry will also be seeing a major digital wave, and technologies such as virtual reality, augmented reality, big data, IoT, and robotics and automation will be integrated. This will help in better, more cost-effective manufacturing techniques and aircraft designs, offering passengers a more personalised experience and better cybersecurity. For instance, airlines can use big data to analyse and predict customer behaviour to generate more personalised offers. This will help increase sales, enhance upselling opportunities, and build better customer relationships. Despite the pandemic, the US airline industry saw no major bankruptcies and proved to investors that it has grown a lot more resilient to external shocks than before. It will take airlines the next two to three years for a full recovery, but it will get there. Investing in airline stocks could be the right strategy for you if you are bullish on the industry prospects and are looking for a long-term investment. The key here is to invest in well-run and well-established carriers, most of which are American. And now, you can access these promising US stocks by downloading the Appreciate app.