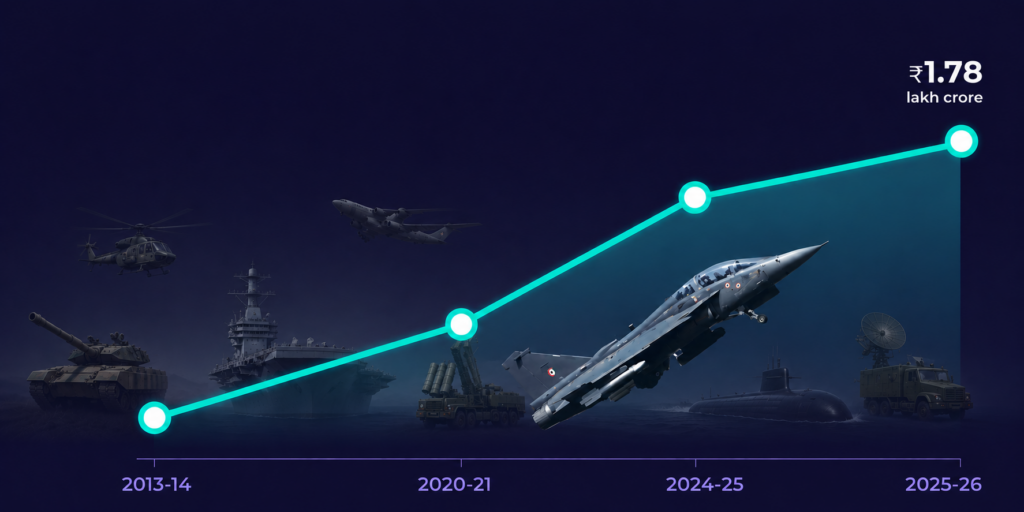

India’s Ministry of Defence announced on June 17, 2026, that the country’s annual defence production reached an all-time high of ₹1.78 lakh crore in the financial year that closed in March 2026, a 15.6% increase over FY25’s ₹1.54 lakh crore, and a 110% increase since FY 2020-21, when production stood at ₹84,643 crore. Viewed across a longer horizon, the growth is even more pronounced: production has nearly quadrupled from ₹43,746 crore in FY 2013-14, the year before the current government’s manufacturing-focused defence policy framework began taking shape.

Defence Minister Rajnath Singh, posting on X, credited what he described as the collective efforts of the Department of Defence Production and both public and private sector partners, framing the trajectory as a clear indicator of the country’s expanding defence industrial base. The announcement triggered an immediate rally in defence-related stocks on the same trading day, with Paras Defence and Space Technologies surging as much as 12% and gains extending across MTAR Technologies, Astra Microwave Products, Data Patterns, Bharat Dynamics, Hindustan Aeronautics, and Bharat Electronics.

The Headline Numbers, Disaggregated

The composition of the ₹1.78 lakh crore figure is where the more interesting story sits. Defence Public Sector Undertakings and other government-owned enterprises accounted for approximately 76% of total production, while the private sector contributed the remaining 24%, a meaningful rise from 22% in FY 2024-25. In absolute terms, private sector contribution reached an all-time high of approximately ₹42,000 crore in FY26.

The framing that several commentators converged on independently is worth stating plainly: a one-percentage-point increase in private sector share sounds incremental, but on a base that has grown 110% in five years, that one point represents real capacity that did not exist at this scale before. India’s defence ecosystem is visibly less dependent on government-run manufacturers than it was even two years ago, even though the structural dominance of DPSUs in absolute output remains intact and is unlikely to reverse in the near term given the scale of platforms, fighter aircraft, submarines, missile systems, that remain concentrated in PSU hands for both technical and strategic reasons.

The production growth has directly fed a parallel export story. Defence exports reached a record ₹38,424 crore in FY26, an increase of more than 62% over the previous year, and a roughly 25-fold increase since FY17. Indian defence products are now reaching more than 80 countries, spanning categories including bulletproof jackets, Dornier Do-228 aircraft, Chetak helicopters, fast interceptor boats, lightweight torpedoes, weapon locating radars, and electronic warfare systems.

The Policy Architecture Behind the Numbers

The growth did not happen by accident, and tracing the specific policy levers explains why the trajectory has been sustained rather than a single good year tied to one large contract.

The Positive Indigenisation Lists are the most structurally important mechanism. These lists, which now cover more than 17,000 items, function as a binding procurement signal: once an item appears on a Positive Indigenisation List, the armed forces are barred from importing it beyond a specified timeline, forcing demand toward domestic manufacturers (both DPSUs and private companies) regardless of whether an imported alternative might be marginally cheaper or faster to acquire in the near term. This demand certainty is what has allowed both established defence PSUs and a growing tier of private manufacturers to commit capital to capacity expansion with confidence that the resulting output has a guaranteed buyer.

Alongside the indigenisation lists, the government has run innovation and startup-focused programmes including iDEX (Innovation for Defence Excellence), ADITI, and SRIJAN, designed specifically to draw smaller private companies and startups into a sector historically dominated by a small number of large PSUs and established private conglomerates. Streamlined procurement procedures under the Defence Acquisition Procedure have reduced the historical multi-year lag between a requirement being identified and a contract being signed, a bottleneck that, as recently as a decade ago, was one of the most frequently cited obstacles to defence manufacturing investment in India.

The fiscal commitment underpinning this policy framework has scaled correspondingly. The defence budget has grown from ₹2.53 lakh crore in FY14 to a projected ₹6.81 lakh crore in FY26, and the Union Budget for FY 2026-27 has allocated approximately ₹7.85 lakh crore to the Ministry of Defence, making it the highest-funded ministry in the central government budget, a 15.19% increase over FY26’s budget estimate, and equivalent to 14.67% of total central government expenditure. Within that allocation, ₹1.39 lakh crore has been specifically earmarked for procurement from domestic defence industries, the budgetary mechanism that converts policy intent into actual production orders. Capital expenditure within the defence budget has crossed ₹2.19 lakh crore. The Defence Research and Development Organisation’s allocation has also risen, from ₹26,816.82 crore in FY26 to ₹29,100.25 crore in FY27, reflecting continued investment in the indigenous technology pipeline that feeds future production.

The Order Book Evidence: What Individual Companies Are Reporting

The aggregate production figure is corroborated, rather than contradicted, by the order book data that India’s listed defence companies have disclosed for FY26, and the scale of that order book pipeline is what is driving the equity market’s continued conviction in the sector despite already-elevated valuations.

Hindustan Aeronautics Limited, India’s largest defence aerospace company, reported an order book of approximately ₹2,54,538 crore as of March 31, 2026, a 34% increase year-on-year from ₹1,89,000 crore, driven substantially by the ₹62,370 crore Light Combat Aircraft Mk1A contract. Fresh order intake for FY26 alone totalled ₹97,028 crore, comprising ₹69,668 crore from manufacturing and ₹26,539 crore from repair and overhaul work. Management has indicated a further potential order inflow opportunity of approximately ₹90,000 crore over the next two years, and has separately signed contracts worth ₹5,083 crore with the Ministry of Defence specifically to strengthen India’s maritime security, alongside a ₹2,901 crore order for six ALH Mk-III maritime helicopters for the Indian Coast Guard. HAL’s FY26 revenue rose to ₹32,250 crore from ₹30,981 crore, and the company has guided for accelerating double-digit revenue growth from FY27 onward as execution on its expanded order book ramps up, targeting an EBITDA margin including other income of 38-39%.

Bharat Electronics Limited, the Navratna-status defence electronics PSU, reported record provisional FY26 turnover of approximately ₹26,750 crore, a 16.2% increase over ₹23,024 crore in FY25. The company secured fresh orders worth around ₹30,000 crore during the year, including export orders valued at $346 million, and its total order book reached approximately ₹74,000 crore as of April 1, 2026, including an export order book of roughly $495 million. BEL’s export sales specifically rose to $141.9 million in FY26 from $106.17 million in FY25, a 33.65% increase. Chairman and Managing Director Manoj Jain explicitly linked the company’s strategic positioning to the geopolitical environment, noting that ongoing tensions in West Asia have reinforced the importance of self-reliance in strategic sectors, a direct reference to the supply chain vulnerabilities the Strait of Hormuz disruption exposed across India’s broader import-dependent industrial base earlier in 2026.

Bharat Dynamics Limited’s order book stood at ₹22,814 crore as of April 1, 2025, with ₹5,909 crore in new orders received during FY26, projecting a year-end order book of approximately ₹26,176 crore as of March 31, 2026, with a further ₹15,000 crore in additional orders still in the pipeline. Mazagon Dock Shipbuilders held an order book of ₹27,415 crore. Garden Reach Shipbuilders & Engineers reported an order book of ₹15,324.13 crore spanning nine projects across 39 platforms, a figure below the ₹20,000 crore mark for the first time in five years, which management characterised as a positive signal of accelerating execution pace rather than a demand weakness.

The Defence Acquisition Council, the apex body that approves major procurement proposals before they convert into formal contracts, approved projects worth ₹2.38 trillion in March 2026 alone, providing a strong forward indicator of the contract pipeline that will convert into production orders, and by extension, into the production figures that will be reported for FY27 and beyond.

Also Read: Best Defence Stocks in India 2026

Reading the Stock Market Reaction

The market’s response to the June 17 announcement, a broad rally across defence-linked equities, reflects accumulated conviction rather than a surprised reaction to genuinely new information, since most of the underlying order book and capacity data has been progressively disclosed by individual companies across their own quarterly results through the year. What the aggregate ₹1.78 lakh crore figure provides is a single, government-sourced confirmation that the sector-wide trend lines documented company-by-company are consistent with the official national data, a form of independent verification that institutional investors weight meaningfully when assessing sector-wide theses.

The valuation context is one that analysts have flagged with increasing frequency as the sector’s multi-year rally has compounded. Bharat Electronics, for instance, has delivered a 921% return over the last five years and trades at a market capitalisation of approximately ₹3,23,311 crore. Hindustan Aeronautics carries a market capitalisation in the range of ₹2.44 to ₹3.32 lakh crore depending on the specific trading session referenced. Several research notes published through 2026 have explicitly cautioned that valuations across the listed defence sector are stretched relative to historical multiples, even as the underlying order books and execution visibility, now extending in HAL’s case to 2034, remain genuinely strong. The standard institutional framing has been to recommend buying on market dips rather than chasing the sector at current multiples, while monitoring the rate at which Acceptance of Necessity approvals (the formal government step preceding a contract) convert into signed orders as the key leading indicator of whether the current order book momentum is sustainable.

The Targets Ahead: ₹3 Lakh Crore and ₹50,000 Crore

The government has articulated explicit forward targets that index the FY26 achievement against a longer-term ambition. The stated goals are to scale annual defence production to ₹3 lakh crore and defence exports to ₹50,000 crore by 2029, targets that, if met, would require defence production to grow by a further 68% from the FY26 base over three years, and exports to grow by approximately 30% over the same period. Separately, some government communications have referenced a $34.7 billion domestic defence manufacturing target by FY29, broadly consistent with the ₹3 lakh crore rupee figure at prevailing exchange rates.

Whether these targets are achieved depends on the same structural variables that have driven the FY26 result: continued conversion of Defence Acquisition Council approvals into signed contracts, sustained private sector capacity investment that pushes the 24% private-sector production share higher over time, and the maintenance of export market access across the more than 80 countries that currently purchase Indian defence equipment, a footprint that itself depends on continued diplomatic and trade relationship management alongside the underlying product quality and pricing competitiveness that have driven the export growth to date.

The geopolitical backdrop provides both tailwind and complication. Global defence spending has risen amid heightened tensions in multiple theatres, creating export opportunity for a country positioning itself as a credible, cost-competitive alternative supplier. At the same time, India’s own experience with the West Asia energy supply disruption earlier in 2026, which exposed the country’s vulnerability to externally controlled supply chains for items as fundamental as crude oil and LPG, has reinforced the strategic logic of self-reliance in defence manufacturing specifically, a sector where import dependence carries national security implications that go beyond the commercial considerations that apply to most other import categories.

Disclaimer: Investments in securities markets are subject to market risks. Read all related documents carefully before investing. The securities and examples mentioned above are only for illustration and are not recommendations.