When Western Digital decided to split itself in two last February, investors barely noticed just another corporate restructuring in a sector they’d learned to ignore. SanDisk would go its own way as a pure flash memory play while the parent kept the hard drive business, and the market shrugged at what seemed like routine financial engineering. Then something remarkable happened. By spring the stock was climbing steadily, by summer it had accelerated, and by November early investors were sitting on 600% gains while Wall Street scrambled to upgrade ratings and institutional money rushed in.

The Shift No One Saw Coming

Memory has always been the unglamorous side of semiconductors, grinding out thin margins in a brutally cyclical business where capacity expansions led to oversupply, oversupply crushed prices, prices recovered, and triggered new expansions in an endless wheel that kept turning. While chip designers captured imaginations and premium valuations, memory makers operated in the shadows as commodity producers that investors learned to trade rather than own. AI broke that pattern completely because training large language models doesn’t just need processing power it devours memory bandwidth at exponential rates, and every data center expansion now hits the same constraint of not enough fast memory to feed the chips doing actual computation.

When demand surged this time supply stayed disciplined because manufacturers had learned painful lessons from previous cycles, so prices held and margins expanded from single digits into double digits while the sector everyone had written off started printing cash.

Related: Top Semiconductor Stocks in USA

Four Companies Capturing the Opportunity

Western Digital posted a remarkable 247% gain in 2025 after spinning off its flash business, emerging as a focused pure-play HDD manufacturer at precisely the moment when hyperscalers needed massive cold storage capacity for AI-generated data archives.

The company’s nearline HDDs, now reaching capacities above 30TB per drive, deliver storage economics that SSDs simply cannot match for long-term data retention, and cloud revenue surged 31.5% year-over-year to account for 89% of total sales while gross margins expanded from sub-30% levels in previous years to 43.5% as pricing power returned to what was once considered a dying technology.

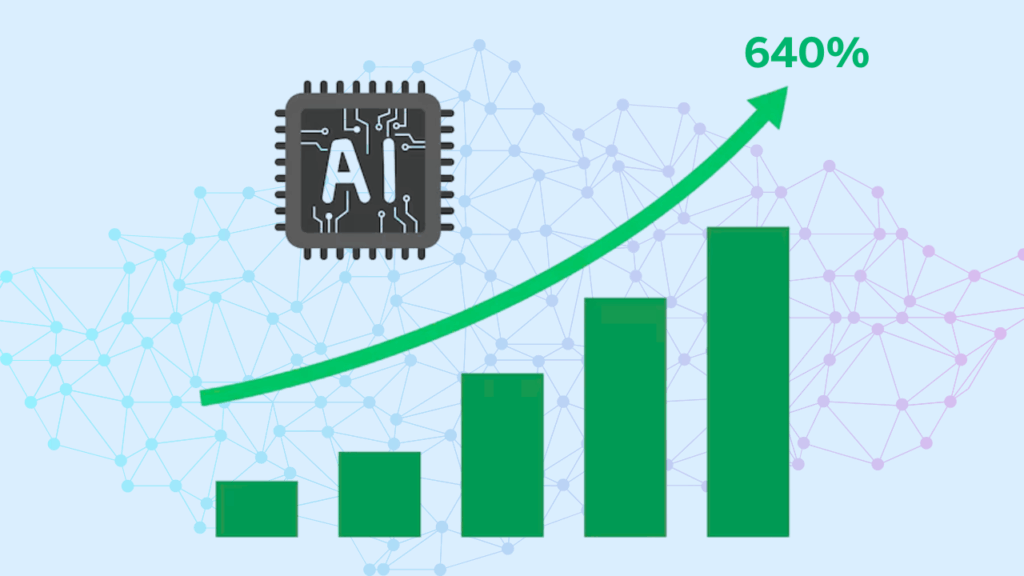

SanDisk emerged from its February spinoff as the year’s most explosive growth story, climbing nearly 640% as investors finally assigned proper value to a pure-play enterprise flash business that had been buried inside Western Digital‘s diversified structure for years.

The company’s proprietary 3D NAND technology and strategic pivot toward enterprise SSDs positioned it as critical infrastructure for AI data pipelines rather than a consumer electronics supplier, with data center revenue jumping from roughly 6% of sales a year ago to 12% as hyperscalers qualified SanDisk’s high-capacity drives for AI workloads that demand both speed and density.

Micron Technology delivered gains exceeding 177% year-to-date while establishing itself as the leading Western supplier of high-bandwidth memory (HBM), the specialized DRAM that sits directly alongside AI accelerators and determines how fast neural networks can train and run inference.

The company’s HBM revenue alone hit $2 billion in fiscal Q4 and data center business now accounts for 56% of total sales, reflecting how AI servers consume exponentially more memory than traditional computing as each new generation of Nvidia and AMD GPUs requires significantly more HBM content than its predecessor, creating automatic pull-through demand that follows every AI chip order placed by hyperscalers.

Read more: 6 U.S. Tech Infrastructure Firms Shaping the Future of AI

Seagate surprised skeptics who predicted HDDs would disappear by posting a 202% year-to-date gain on the realization that tiered storage architectures mixing fast SSDs for active data with cheap HDDs for archives optimize both performance and economics at cloud scale.

The company’s HAMR technology enables drives reaching 44TB capacity with a roadmap to 50TB and beyond, addressing cold storage needs where cost per terabyte matters more than access speed, and mass capacity revenue jumped 40% year-over-year as cloud providers discovered that AI generates far more historical data requiring long-term storage than anyone anticipated when they were building infrastructure for traditional workloads.

What Indian Investors Need to Understand

Indian investors can access all four companies with as little as ₹1 through fractional investing without large capital requirements or complexity, including through platforms like Appreciate that simplify access to US-listed tech names. For investors researching how to invest in US stocks from India, fractional investing platforms provide an accessible way to gain exposure to global technology leaders without requiring significant capital.

What matters more, though, is understanding the cyclical nature of memory markets, because these businesses will face supply-demand imbalances again. The investment case depends on believing that AI and cloud computing create structural demand growth overwhelming cyclical volatility, compelling if you’re thinking in years rather than quarters, even as currency swings add another layer of movement that investors on Appreciate and similar platforms increasingly factor into their decisions.

Related: Top Technology Stocks in USA

The Opportunity Ahead

SanDisk’s surge revealed how drastically investors had mispriced memory when they treated it as commodity manufacturing, and separating flash from hard drives forced a revaluation where suddenly the market could see what each business was worth serving AI infrastructure. The pattern repeated across the sector as Western Digital rallied, Micron climbed steadily and even Seagate found respect, because memory lacks the narrative excitement of AI chips or frontier models but infrastructure ultimately matters more than stories and memory has become the infrastructure making AI economics work. That’s the hidden opportunity in 2025 not hidden because it’s secret but because it sits one layer below where most investors look, with proven companies holding defensible technology and fundamentally improved market positioning that seemed mature a year ago but now looks like the early phase of a multi-year expansion with structural margin improvements intact.

Disclaimer: Investments in securities markets are subject to market risks. Read all the related documents carefully before investing.